În fiecare lună, angajatorul este obligat să plătească prime de asigurare pentru fiecare dintre angajații săi. Se plătesc în plus față de salariul lunar și pe cheltuiala angajatorului. Prin aceasta se deosebesc de impozitul pe venitul personal de 13%, pe care angajatul il plateste lunar din propriul buzunar, iar angajatorul actioneaza doar ca agent fiscal si vireaza acesti bani la buget.

Anterior, angajatorul plătea contribuții într-o singură plată la impozitul social unificat, care mobiliza fondurile cetățenilor pentru viitoarea lor pensie, asigurări sociale și îngrijiri medicale. Cota de impozitare a fost de 26%. După eliminarea impozitului social unificat, primele de asigurare au început să fie plătite separat către Fondul de pensii, Fondul de asigurări sociale și Fondul federal de asigurări medicale obligatorii. Dar acest lucru nu schimbă esența deducțiilor. Din 2011, valoarea totală a contribuțiilor a crescut la 34% din cauza creșterii contribuțiilor la pensie. Acest lucru a dus la o creștere a plăților gri și la o scădere a colectării impozitelor, apoi s-a luat decizia de reducere a primelor de asigurare. În 2013-2014 mărimea lor era de 30% din salariul oficial al angajatului.

Distribuirea primelor de asigurare

Primele de asigurare sunt repartizate după cum urmează. 22% din salariul angajatului merge la Fondul de pensii; acești bani sunt luați în considerare în contul personal de pensie al cetățenilor și ulterior servesc drept bază pentru formarea viitoarei pensii. Anterior, aceste fonduri erau distribuite părților finanțate și asigurărilor din pensie, dar acum toate plățile sunt creditate în partea de asigurări. Pentru a păstra partea finanțată, angajatul trebuie să-și transfere economiile către Fondul de pensii nestatal.

5,1% este transferat către asigurările de sănătate ale angajaților (la Fondul Federal de Asigurări Medicale Obligatorii). Alte 2,9% merg la asigurările sociale din Fondul de asigurări sociale. Acest fond, în special, este responsabil pentru plățile de asigurare pentru invaliditate temporară și concediu. Astfel de tarife sunt valabile până când angajatul atinge un nivel anual de venit de 624 de mii de ruble. Când se ajunge la această sumă, angajatorul plătește 10% la Fondul de pensii, iar plățile rămase ajung la 0%.

Unii angajatori au beneficii atunci când plătesc prime de asigurare. Ei plătesc impozite pe salarii la Fondul de pensii cu o rată de 20%, dar nu plătesc la Fondul federal de asigurări medicale obligatorii. Este vorba, de exemplu, de farmacii pe UTII, companii și antreprenori individuali pe sistemul fiscal simplificat angajați în construcții, producție alimentară, producție de îmbrăcăminte etc.

Nu contează dacă angajatul lucrează în baza unui contract de muncă sau în cadrul unui contract de drept civil sau al dreptului de autor. Toate contribuțiile la Fondul de pensii și la Fondul federal de asigurări medicale obligatorii sunt transferate integral. Singurul lucru este că angajatorul în acest caz nu este obligat să facă plăți către Fondul de Asigurări Sociale (dar, cu toate acestea, poate face acest lucru).

Forma de proprietate a angajatorului nu contează. Atât antreprenorii individuali, SRL-urile, cât și OJSC-urile plătesc impozite pe salarii în conformitate cu procedura stabilită.

Calculul primelor de asigurare

De exemplu, salariul oficial al unui angajat este de 25.000 de ruble. În fiecare lună (până în a 15-a zi de la plată), angajatorul trebuie să transfere 22% la Fondul de pensii (25.000 * 0,22) sau 5.500 de ruble, 5,1% la FFOMS (25.000 * 0,051) sau 1.275 de ruble. și 2,9% în Fondul de asigurări sociale (25000*0,029) sau 725 de ruble.

Rezultă că costul lunar al fiecărui angajat îl costă pe angajator cu 30% mai mult decât salariul său.

UST - Impozitul social unificat. Deși a fost desființat încă din 2010, mulți sunt obișnuiți să numească contribuțiile sociale pe vechiul mod - UST. Cred că aproape fiecare contabil care se ocupă de salarizare este familiarizat cu metodologia de calcul a deducerilor pentru Taxa Socială Unificată și nu pare să fie atât de complicată, dar pe de altă parte, calcularea acestui impozit pentru fiecare angajat separat nu este atât de simplă. . Chestia este că acest impozit trebuie plătit lunar, iar baza de impozitare pentru calculul impozitului social unificat se determină pe baza venitului efectiv acumulat angajatului. total cumulat. Acestea. în fiecare lună de raportare ulterioară a perioadei financiare, este necesar să se țină cont de veniturile lunilor anterioare ale acestei perioade. Și, în funcție de mărimea tuturor taxelor, tariful UST poate fi modificat. Mai precis, mărimea cotei UST ar trebui redusă dacă suma totală a angajărilor către angajat pentru perioada financiară de raportare a depășit dimensiunea bazei de impozitare stabilită de Codul Fiscal. Eu numesc această dimensiune pragul. Până în 2014, au existat 2 astfel de praguri: primul prag a fost de 280.000 de ruble, al doilea de 600.000 de ruble. Pe baza acestui fapt, tarifele UST s-au modificat după cum urmează:

- Dacă valoarea angajamentelor este mai mică de 280.000 de ruble, atunci rata este de 30%

- Dacă valoarea angajamentelor a fost mai mare de 280.000 de ruble, dar mai mică de 600.000 de ruble. - rata se reduce la 10%

- Dacă valoarea angajamentelor depășește 600.000 de ruble. - rata se reduce la 2%

Cu toate acestea, în 2014 tarifele s-au modificat și a rămas un singur prag:

- Dacă valoarea angajamentelor este mai mică de 624.000 de ruble, atunci rata este de 30%

- Dacă valoarea angajamentelor depășește 624.000 de ruble, atunci rata este redusă la 10%

În 2015, tarifele s-au schimbat, s-a decis să se lase pragul la fel, dar a devenit necesară defalcarea deducerilor:

- Dacă valoarea angajamentelor a fost mai mică de 711.000 de ruble, atunci rata este de 27,1% (22% în Fondul de pensii al Federației Ruse și 5,1% în Fondul federal de asigurări medicale obligatorii)

- Dacă valoarea angajamentelor depășește 711.000 de ruble, atunci rata este redusă la 15,1% (10% în Fondul de pensii al Federației Ruse și 5,1% în Fondul federal de asigurări medicale obligatorii)

În 2016, tarifele s-au schimbat din nou, iar pentru Fondul de pensii și Fondul de asigurări sociale diferă:

- Fond de pensie- Dacă valoarea angajamentelor a fost mai mică de 796.000 de ruble, atunci rata este de 22%, dacă a depășit 796.000 de ruble. - 10%

- FSS- Dacă valoarea angajamentelor a fost mai mică de 718.000 de ruble, atunci rata este de 2,9%, dacă a depășit 718.000 de ruble. - 0%

Pragurile în sine nu sunt o problemă de luat în considerare. Dar dacă pragul a fost depășit la „mijlocul salariului”, atunci o parte din salariu înainte de depășirea pragului este impozitată cu o cotă de 27,1%, iar a doua - 15,1%, ceea ce este logic. Acest lucru creează probleme suplimentare la calcularea părții fiscale - calculul acestor praguri pentru fiecare lună.

De exemplu, un angajat primește 100.000 de ruble lunar. În prima lună, dimensiunea UST ar trebui să fie de 27,1% din venit, adică. 27.100 RUB În a doua lună, valoarea angajamentelor va fi deja de 200.000 de ruble, ceea ce este mai mică decât pragul de 711.000 de ruble, astfel încât rata UST va rămâne de 27,1%, adică. aceleași 27.100 de ruble. Și așa în primele 7 luni. Cu toate acestea, în luna a 8-a, suma totală a deducerilor va fi de 800.000 de ruble, ceea ce depășește 711.000 de ruble. iar rata ar trebui redusă la 15,1%. Dar 11.000 de ruble. din 100.000 de ruble. pentru a 8-a lună sunt încă supuse unei rate de 27,1%, iar restul de 89.000 de ruble. deja la o rată redusă de 15,1%. Prin urmare, UST pentru a 8-a lună va fi: (11.000 * 27,1%) + (89.000 * 15,1%), ceea ce va avea ca rezultat o sumă UST egală cu 16.420 de ruble. În lunile următoare, valoarea taxei va fi de 15,1% din taxe, adică. 15.100 RUB

Dar salariile, de regulă, sunt diferite pentru fiecare și nu atât de „chiar” (100.000). Și dacă nu există programe specializate la îndemână, atunci calcularea impozitului social unificat devine o sarcină destul de lungă.

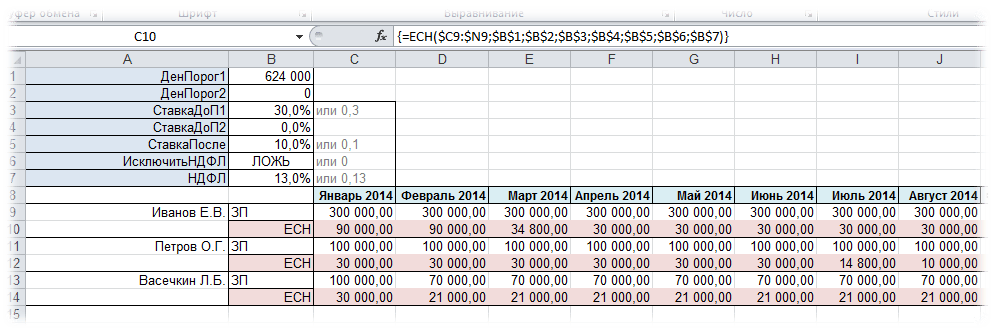

Funcţie UST vă va ajuta să calculați acest impozit rapid și fără probleme. Ea ține cont de toate aceste nuanțe și calculează valoarea impozitului necesar pentru deduceri pentru fiecare lună. În acest caz, puteți specifica până la două sume de prag, ceea ce asigură că funcția poate fi utilizată în viitor.

În cazul împărțirii contribuțiilor (în contribuții la Fondul de pensii la o rată și la Fondul de asigurări sociale cu alta), funcția trebuie aplicată de două ori - o dată indicând valorile prag pentru Fondul de pensii și a doua oară pentru valorile de prag ale Fondului de Asigurări Sociale. Apoi, dacă este necesar, rezultatele pot fi rezumate.

Tot ceea ce trebuie specificat pentru a utiliza funcția sunt datele privind venitul lunar al angajaților, sumele de prag, ratele dobânzilor înainte și după depășirea pragului. De asemenea, puteți indica în plus excluderea impozitului pe venitul personal din calcul și procentul impozitului pe venitul personal dacă acesta se modifică brusc. În mod implicit, indicarea sa este opțională și este egală cu 13%.

Apelarea unei comenzi printr-un dialog standard:

Apel de la panoul MultEX:

Sumă/Căutare/Funcții - Financiar - UST

Sintaxă:

=ESH($C6:$N6, $B$1, $B$2, $B$3, $B$4, $B$5)

=ESH($C6:$N6, $B$1, $B$2, $B$3, $B$4, $B$5, TRUE, $B$7)

=UST($C6:$N6; 711000; 0; 0,271; 0,151; 0; 1; 13%)

Sursa de venit($C6:$N6) - indică intervalul de celule în care sunt înregistrate sumele de venit pentru perioada respectivă. Intervalul poate fi o coloană sau un rând. Fiecare celulă trebuie să conțină suma venitului pentru o lună.

Den Threshold1($B$1) - indică celula cu suma sau suma venitului total al angajatului, ceea ce va însemna primul prag, după depășirea căruia se reduce cota de impozitare.

Den Threshold2($B$2) - indică celula cu suma sau suma venitului total al angajatului, ceea ce va însemna al doilea prag, după depășirea căruia cota de impozitare se reduce a doua oară. Dacă se aplică un singur prag, atunci acesta trebuie specificat ca argument Den Threshold1, și argumentul Den Threshold2 atribuiți valoarea 0. Atunci pur și simplu nu va fi luată în considerare de funcție.

RateDoP1($ B$ 3) - este indicată o celulă cu un număr sau un număr în sine, indicând procentul utilizat pentru anularea impozitului dacă venitul total al angajatului pentru perioada nu depășește valoarea DayThreshold1. Este permisă specificarea unei referințe la o celulă cu un procent sau un număr, sau constante directe: 30%, 0,3 (pentru localizarea în limba rusă) și 0,3 (pentru localizarea în limba engleză).

RateDoP2($B$4) - indică o celulă cu un număr sau un număr care indică direct procentul utilizat pentru anularea impozitului dacă venitul total al angajatului pentru perioada este mai mare decât suma specificată în Den Threshold1și nu depășește suma specificată în Den Threshold2. Este permisă specificarea unei referințe la o celulă cu un procent sau un număr sau constante directe: 30%, 0,3 (pentru localizarea în limba rusă) și 0,3 (pentru localizarea în limba engleză). Dacă este utilizat un singur prag pentru a calcula UST și DenThreshold2 i se atribuie valoarea 0, RateDoP2 nu se aplica.

RateAfter($B$5) - este indicată o celulă cu un număr sau un număr propriu-zis, indicând procentul utilizat pentru anularea impozitului dacă venitul total al angajatului pentru perioada a depășit suma DenThreshold1 (în cazul utilizării a două praguri - DenThreshold2) . Este permisă specificarea unei referințe la o celulă cu un procent sau un număr sau constante directe: 10%, 0,1 (pentru localizarea în limba rusă) și 0,1 (pentru localizarea în limba engleză).

Excludeți impozitul pe venitul personal(ADEVĂRAT) - Opțional. Este indicat logic ADEVĂRAT sau FALS. Dacă este specificat ADEVĂRAT sau 1 , apoi la calcularea venitului total al angajatului se va deduce din venit suma impozitului pe venitul personal (implicit 13%). Dacă este specificat FALS, 0 sau argumentul este omis, atunci impozitul pe venitul personal nu va fi dedus la calcularea venitului total al angajatului. Implicit la FALS.

Impozitul pe venitul personal($ B$ 7) - Opțional. Referință de celulă sau constantă. Marimea este indicata Impozitul pe venitul personal ca procent - 13% (sau 0,13). Se aplică numai dacă argumentul Excludeți impozitul pe venitul personal enumerate ca ADEVĂRAT. În caz contrar, procentul nu se aplică.

Mai multe despre locația datelor. Datele acumulate trebuie înregistrate pe un rând sau coloană și trebuie să fie în ordine cronologică, fără săriți luni. Un exemplu de aranjare a datelor pe orizontală (în rând) - Opțiunea 1:

Aranjarea datelor pe orizontală (în rând) - Opțiunea 2:

Aranjarea datelor pe verticală (într-o coloană):

Impozitul Social Unificat este o inovație serioasă inclusă în partea a doua a Codului Fiscal. Promulgată la 1 ianuarie 2001, această taxă a înlocuit contribuțiile existente anterior la trei fonduri sociale extrabugetare de stat - Fondul de pensii, Fondul de asigurări sociale și fondurile federale și regionale de asigurări obligatorii de sănătate. Însă înlocuirea deducerilor cu un singur impozit social nu a anulat scopul propus al impozitului. Fondurile din colectarea acesteia nu vor merge la bugetele de toate nivelurile, ci la fondurile indicate mai sus. Scopul principal al acestei taxe este tocmai acela de a asigura mobilizarea fondurilor pentru realizarea dreptului cetățenilor ruși la pensie de stat și asigurări sociale și asistență medicală.

Scopul Taxei Sociale Unificate este simplificarea procedurii de colectare a fondurilor, simplificarea mecanismului de calcul al primelor de asigurare, uniformizarea bazei de impozitare, reducerea raportarii, introducerea unei proceduri uniforme de aplicare a sanctiunilor financiare si reducerea numarului de cecuri ale platitorilor, precum și să ușureze presiunea fiscală asupra fondului de salarii și din acest motiv să legalizeze parțial câștigurile mari și să ușureze impozitarea veniturilor din muncă.

Taxa socială unificată se plătește de la 01/01/2001 în conformitate cu partea a doua a Codului fiscal al Federației Ruse, aprobată prin Legea federală din 05/08/2000 nr. 117-FZ și pusă în vigoare la 01/01 /2001 prin Legea federală din 05/08/2000 nr. 118-FZ „Cu privire la intrarea în vigoare partea a doua a Codului fiscal al Federației Ruse și modificările unor acte legislative ale Federației Ruse privind impozitele”.

Din 2010, impozitul social unificat a fost desființat, în schimb, contribuabilii actuali vor plăti contribuții de asigurare la Fondul de pensii, la Fondul de asigurări sociale, la fondurile federale și teritoriale de asigurări medicale obligatorii, în conformitate cu Legea nr. 213-FZ din 24 iulie 2009. . Ratele totale de deducere nu s-au modificat de la 1 ianuarie 2010.

Plătitorii impozitului social unic sunt uniți în două grupe, pentru fiecare dintre acestea fiind stabilit un obiect de impozitare independent.

Prima grupă de contribuabili include angajatorii care efectuează plăți către angajați:

organizații;

Persoane fizice care nu sunt recunoscute ca antreprenori individuali.

Al doilea grup de contribuabili include neangajatorii:

Antreprenori individuali;

Avocați.

Membrii unei întreprinderi țărănești (ferme) sunt tratați ca întreprinzători individuali.

Dacă un contribuabil aparține simultan la două dintre grupurile enumerate, atunci el este recunoscut ca contribuabil pe fiecare bază individuală.

Sunt scutite de la plata impozitului social unic:

1. Organizații de orice formă organizatorică și juridică cu sume de plăți și alte remunerații care nu depășesc 100 de mii de ruble în perioada fiscală. pentru fiecare angajat care este persoană cu handicap din grupa I, II sau III.

2. Angajatorii cu sume de plăți și alte remunerații care nu depășesc 100 de mii de ruble. în perioada fiscală pentru fiecare angajat individual. Acestea includ:

a) organizațiile publice ale persoanelor cu dizabilități (inclusiv cele create ca uniuni ale organizațiilor publice ale persoanelor cu handicap), dintre ai căror membri persoanele cu handicap și reprezentanții legali ai acestora formează cel puțin 80%, filialele lor regionale și locale;

b) organizațiile al căror capital autorizat este constituit integral din contribuții de la organizațiile publice ale persoanelor cu handicap și în care numărul mediu de persoane cu handicap este de cel puțin 50%, iar ponderea salariilor persoanelor cu handicap în fondul de salarii este de cel puțin 25%;

c) instituții create pentru a atinge scopuri educaționale, culturale, medicale și recreative, de educație fizică și sport, științifice și alte scopuri sociale etc.

Aceste beneficii nu se aplică contribuabililor implicați în producția și (sau) vânzarea de bunuri accizabile, materii prime minerale, alte minerale, precum și alte bunuri în conformitate cu lista aprobată de Guvernul Federației Ruse la propunerea tuturor. -organizații publice ruse ale persoanelor cu dizabilități;

3. Contribuabilii nu sunt angajatori care sunt persoane cu handicap din grupele I, II sau III, din punct de vedere al veniturilor din activitățile lor antreprenoriale sau din alte activități profesionale în valoare care nu depășește 100 de mii de ruble. în perioada fiscală.

4. Fonduri rusești pentru sprijinirea educației și științei - din sumele plăților către cetățenii Federației Ruse sub formă de granturi (asistență gratuită) acordate profesorilor, lectorilor, elevilor, studenților și (sau) studenților absolvenți ai statului și (sau) instituții de învățământ municipale.

Particularitatea impozitului social unificat este că are nu unul, ca de obicei, ci mai multe obiecte de impozitare stabilite pentru diferite categorii de contribuabili.

1. Pentru contribuabili - angajatori (cu excepția angajatorilor - persoane fizice), obiectul impozitării îl constituie plățile și alte remunerații acumulate de angajatori în favoarea angajaților din toate motivele, inclusiv remunerația (cu excepția remunerațiilor plătite întreprinzătorilor individuali) în temeiul contractelor de drept civil, al cărui subiect este prestarea muncii (prestarea de servicii), precum și în temeiul acordurilor de drepturi de autor și de licență.

2. Pentru contribuabili - persoane fizice care nu sunt recunoscute ca întreprinzători individuali, obiectul impozitării îl constituie plățile și alte remunerații în temeiul contractelor de muncă și de drept civil, al căror obiect este prestarea muncii, prestarea de servicii, plătite de contribuabili în favoarea a indivizilor. Plățile efectuate în cadrul contractelor civile, al căror subiect este transferul de proprietate sau alte drepturi de proprietate asupra proprietății (drepturi de proprietate), precum și contractele legate de transferul de proprietate (drepturi de proprietate) în folosință, nu se aplică pentru obiectul impozitării.

3. Pentru contribuabilii care nu sunt angajatori, obiectul impozitării îl constituie veniturile din activități de întreprinzător sau din alte activități profesionale minus cheltuielile aferente extragerii acestora.

Pentru contribuabilii care sunt membri ai unei întreprinderi (agricole) țărănești (inclusiv conducătorul unei întreprinderi țărănești (agricole), cheltuielile efectiv suportate de întreprinderea menționată legate de dezvoltarea întreprinderii țărănești (ferme) sunt excluse din venituri.

Plățile și remunerațiile specificate la paragraful 1 (indiferent de forma în care sunt efectuate) nu sunt recunoscute ca obiect de impozitare dacă:

Pentru organizațiile de contribuabili, astfel de plăți nu sunt clasificate drept cheltuieli care reduc baza de impozitare pentru impozitul pe profit în perioada curentă de raportare (de impozitare);

Pentru contribuabilii - antreprenori individuali sau persoane fizice, astfel de plăți nu reduc baza de impozitare a impozitului pe venitul persoanelor fizice în perioada de raportare (de impozitare) curentă.

Contribuabili - angajatorii determină baza de impozitare pentru fiecare angajat de la începutul perioadei de impozitare la sfârșitul fiecărei luni pe baza de angajamente (în acest caz, este prevăzută contabilitatea individuală). La sfârşitul perioadei fiscale se calculează baza de impozitare integrală.

Contribuabilii care nu sunt angajatori calculează baza de impozitare din sumele veniturilor încasate în perioada fiscală, atât în numerar, cât și în natură, minus costurile aferente extragerii acestora.

La determinarea bazei de impozitare a impozitului social unificat nu sunt luate in considerare anumite tipuri de plati, venituri, costul serviciilor prestate etc. Pentru majoritatea articolelor, sumele care nu sunt supuse impozitării coincid cu sumele neincluse în venituri luate în considerare la stabilirea impozitului pe venitul persoanelor fizice. Spre deosebire de actele legislative anterioare, aceste beneficii sunt caracterizate de o orientare socială mai largă. Sumele care nu sunt supuse impozitării sunt enumerate la articolul 238 din Codul fiscal.

Perioada fiscală pentru impozitul social unificat este un an calendaristic. Perioadele de raportare fiscală sunt primul trimestru, șase luni și nouă luni ale anului calendaristic.

Cotele de impozitare (Tabelul 1, Tabelul 2) și distribuția acestora sunt determinate de articolul 241 din Codul Fiscal al Federației Ruse.

Diferențierea cotelor unice de impozitare socială pentru contribuabili - angajatori și contribuabili - neangajați este cauzată de diferențele dintre obiectele de impozitare.

Tabel 1. Cote unificate de impozitare socială pentru principala categorie de contribuabili - angajatori care efectuează plăți către angajați

Tabelul 2. Cotele impozitului social unic pentru persoanele angajate în activități antreprenoriale și alte activități profesionale (cu excepția avocaților)

Cotele impozitului social unic sunt diferențiate pe fond. Tariful obișnuit este pentru un angajat cu un venit anual mai mic de 280 de mii de ruble. -- este de 26%. Un exemplu tipic de distribuire a acestor bani pentru un astfel de angajat arată astfel:

· Fondul de pensii al Federației Ruse - 14%

· Bugetul federal - 6,0% (20%? 14%, conform articolului 243, partea 2 din Codul fiscal al Federației Ruse)

· Fondul de asigurări sociale al Federației Ruse - 2,9%

· Fonduri de asigurări obligatorii de sănătate -- 3,1%

Toate procentele afișate se referă la salarii înainte ca impozitele pe venit să fie deduse din acestea.

Se stabilesc cote de impozitare preferențiale pentru organizațiile producătoare de produse agricole, întreprinderile țărănești (agricole), precum și pentru comunitățile de clan și familii ale popoarelor mici din Nord angajate în sectoarele economice tradiționale. Pentru contribuabilii din grupa a doua - neangajatori, cotele impozitului social unic sunt mai mici decât pentru contribuabilii - angajatori.

Sunt stabilite cote de impozitare ușor diferite pentru avocații care oferă asistență juridică gratuită persoanelor fizice.

Potrivit paragrafului 3 al art. 243 din Codul fiscal al Federației Ruse Declarația fiscală se depune de către contribuabil până la data de 30 martie a anului următor perioadei fiscale expirate.

Contribuabilii-angajatorii efectuează plăți de impozit în avans lunar în termenul stabilit pentru primirea fondurilor de la bancă pentru salariile din ultima lună, dar nu mai târziu de data de 15 a lunii următoare.

Contribuabilii care nu sunt angajatori sunt obligați să efectueze plăți în avans pe baza notificărilor fiscale:

Pentru ianuarie - iunie - nu mai târziu de 15 iulie a anului curent în valoare de jumătate din suma anuală a plăților în avans;

Pentru iulie - septembrie - nu mai târziu de 15 septembrie a anului curent în valoare de o pătrime din suma anuală a plăților în avans;

Pentru octombrie - decembrie - nu mai târziu de 15 ianuarie a anului următor în valoare de o pătrime din suma anuală a plăților în avans.

Contribuabilul reflectă date despre sumele plăților anticipate calculate și plătite, date despre valoarea deducerii fiscale utilizate de contribuabil, precum și despre sumele primelor de asigurare efectiv plătite pentru aceeași perioadă în calculul transmis cel târziu la data de 20. zi a lunii următoare perioadei de raportare, către autoritatea fiscală într-o formă aprobată de Ministerul Taxe și Taxe al Federației Ruse.

Diferența dintre sumele plăților în avans plătite în perioada fiscală și suma impozitului de plătit la sfârșitul perioadei fiscale trebuie plătită de către contribuabil până la data de 15 iulie a anului următor perioadei fiscale de raportare. Această sumă poate fi compensată cu plățile viitoare de impozite sau rambursată contribuabilului.

Plata impozitului (plăți în avans) se efectuează prin ordine de plată separate către Fondul de pensii, Fondul de asigurări sociale, Fondul federal de asigurări medicale obligatorii și fondurile teritoriale de asigurări medicale obligatorii.

Un exemplu de calcul al plăților în avans în cadrul Taxei Sociale Unificate

Director general al organizației de construcții Alfa CJSC A.V. Lvov primește un salariu de 55.000 de ruble. pe luna. Salariul managerului A.S. Kondratiev este de 35.000 de ruble. Pentru ianuarie-iulie 2008, organizația în ansamblu a acumulat o plată în avans în cadrul UST în valoare de 147.000 de ruble, inclusiv: - UST către bugetul federal - 113.295 de ruble; - contribuții la Fondul de asigurări sociale din Rusia - 16.275 de ruble; - contribuții la FFOMS - 6405 ruble; - contribuții la TFOMS - 11.025 ruble. Contabilul Alpha a calculat avansul în temeiul Taxei Sociale Unificate pentru august 2008. Baza de impozitare pentru Lviv pentru 8 luni din 2008 s-a ridicat la 440.000 de ruble. (55.000 RUB = 8 luni). Se încadrează în al doilea interval al scalei regresive (de la 280.001 de ruble la 600.000 de ruble). În consecință, plata în avans în cadrul Taxei Sociale Unificate pentru 8 luni în Lviv s-a ridicat la 88.800 de ruble. (72.800 RUB + (440.000 RUB - 280.000 RUB) ? 10%), inclusiv: - Taxa socială unificată la bugetul federal - 68.640 RUB. (56.000 rub. + (440.000 rub. - 280.000 rub.) ? 7,9%); - contribuții la Fondul de asigurări sociale din Rusia - 9720 de ruble. (8.120 RUB + (440.000 RUB - 280.000 RUB) ? 1%); - contribuții la FFOMS - 4040 de ruble. (3.080 rub. + (440.000 rub. - 280.000 rub.) ? 0,6%); - contribuții la TFOMS - 6400 de ruble. (5.600 de rub. + (440.000 de rub. - 280.000 de rub.) ? 0,5%). Baza de impozitare pentru Kondratiev pentru 8 luni din 2008 s-a ridicat la 280.000 de ruble. (35.000 de ruble? 8 luni). Se încadrează în primul interval al scalei regresive (până la 280.000 de ruble). În consecință, plata în avans în cadrul impozitului social unificat pentru 8 luni, conform lui Kondratiev, s-a ridicat la 72.800 de ruble. (280.000 RUB ? 26%), inclusiv: - Taxa socială unificată la bugetul federal - 56.000 RUB. (280.000 RUB - 20%); - contribuții la Fondul de asigurări sociale din Rusia - 8120 de ruble. (280.000 RUB - 2,9%); - contribuții la FFOMS - 3080 de ruble. (280.000 RUB - 1,1%); - contribuții la TFOMS - 5600 de ruble. (280.000 RUB ? 2%). Valoarea totală a plății în avans în cadrul Taxei sociale unificate pentru 8 luni din 2008 la Alfa a fost de 161.600 de ruble. (88.800 RUB + 72.800 RUB), inclusiv: - Taxa socială unificată la bugetul federal - 124.640 RUB. (68.640 RUB + 56.000 RUB); - contribuții la Fondul de asigurări sociale din Rusia - 17.840 de ruble. (9720 rub. + 8120 rub.); - contribuții la FFOMS - 7120 ruble. (4040 rub. + 3080 rub.); - contribuții la TFOMS - 12.000 de ruble. (6400 rub. + 5600 rub.). Plata în avans în temeiul impozitului social unificat plătibilă pentru august 2008 s-a ridicat la 14.600 de ruble. (161.600 de ruble - 147.000 de ruble), inclusiv: - Taxa socială unificată la bugetul federal - 11.345 de ruble. (124.640 RUB - 113.295 RUB); - contribuții la Fondul de asigurări sociale al Rusiei - 1565 de ruble. (17.840 RUB - 16.275 RUB); - contribuții la FFOMS - 715 ruble. (7.120 RUB - 6.405 RUB); - contribuții la TFOMS - 975 de ruble. (12.000 RUB - 11.025 RUB).

Controlul asupra corectitudinii calculului, completității și oportunității contribuțiilor la fondurile sociale extrabugetare de stat plătite ca parte a impozitului social unificat este efectuat de autoritățile fiscale ale Federației Ruse.

Un control fiscal la fața locului se efectuează pe baza unei decizii a șefului (șefului adjunct) al autorității fiscale pe teritoriul (sediul) contribuabilului (clauza 1 a articolului 89 din Codul fiscal al Federației Ruse). . Un audit fiscal la fața locului poate acoperi doar trei ani calendaristici de activitate a contribuabilului imediat anterior anului auditului (Partea 2, Clauza 4, Articolul 89 din Codul Fiscal al Federației Ruse).

Când se pregătește pentru o inspecție, trebuie întocmit un program (plan) pentru implementarea acesteia. Programul (planul) de inspecție este o listă de probleme care trebuie clarificate în timpul inspecției viitoare. Programele de inspecție pentru anumite tipuri de impozite includ aspecte legate de calcularea acestor taxe (Tabelul 3).

Tabelul 3. Plan de audit fiscal

|

Întrebări de verificare |

Documente verificate |

|

Verificarea corectitudinii calculului bazei impozabile a impozitului social unificat |

Extras, jurnal de comandă, registru general, ordine de politică contabilă |

|

Verificarea aplicării corecte a cotelor unificate de impozitare socială |

Extrase de cont, jurnale de comenzi, ordine de politici contabile |

|

Verificarea corectitudinii calculelor sumelor impozitului social unificat |

Declaratiilor fiscale |

|

Verificarea aplicarii beneficiilor la calcularea si plata impozitului social unificat |

Declaratiilor fiscale |

|

Verificarea caracterului complet și oportunității plății impozitului social unitar la buget |

Gazeta, jurnal - ordin pentru contul 51, ordine de plata |

|

Verificarea corectitudinii înregistrărilor contabile pentru acumularea și plata impozitului social unificat la buget |

Extras, jurnal de comandă, registru general |

|

Verificarea corectitudinii întocmirii și transmiterii la timp a rapoartelor privind impozitul social unificat către organele fiscale |

Declaratiilor fiscale |

|

Verificarea corectitudinii contabilitatii analitice si sintetice |

Extrase de cont, jurnal comenzi, Registrul mare, bilant |

În procesul de efectuare a unui audit, angajații inspectoratului fiscal, pe baza informațiilor de care dispune inspectoratul despre activitățile contribuabilului, a datelor din documentele furnizate acestora, a materialelor primite în timpul acțiunilor de audit:

Analizează toate informațiile disponibile despre activitățile contribuabilului auditat;

Ele identifică neconcordanțe în conținutul documentelor studiate, încălcări ale procedurilor contabile, întocmirea declarațiilor fiscale și analizează impactul acestor încălcări asupra formării bazei de impozitare;

Formați o bază de probă pe faptele infracțiunilor fiscale identificate;

Aceștia calculează sumele impozitelor și penalităților neplătite de către contribuabil și formulează propuneri de tragere la răspundere a contribuabilului pentru săvârșirea de infracțiuni fiscale, precum și de eliminare a încălcărilor identificate.

Rolul și semnificația Taxei Sociale Unificate este mare. Însuși numele impozitului și direcția de utilizare a fondurilor indică faptul că, cu ajutorul ei, se rezolvă probleme stringente ale vieții oamenilor și în special ale fiecărei persoane. Realizarea principalelor obiective ale reformelor realizate în țară și atenuarea problemelor acute emergente de natură socială, printre care: asigurarea unei pensii decente, stimularea unei politici demografice eficace, inclusiv creșterea speranței de viață a națiunii, depinde în mare măsură de modul în care fondurile colectate prin impozitul social unificat vor fi acumulate.prin îngrijiri medicale calificate în timp util, creând condiții pentru munca normală și odihnă.

Fără îndoială, UST a fost pasul corect și justificat în organizarea legislației fiscale, dar a necesitat îmbunătățiri.

Scara regresivă a cotelor de impozitare UST și condițiile de aplicare a acesteia au dezavantaje semnificative. Condițiile de aplicare a ratelor regresive sunt prea stricte, iar numărul organizațiilor care le pot folosi este foarte limitat. UST este un impozit pentru persoanele juridice, dar contribuabilul este obligat să țină un cont personal cu toate plățile pentru fiecare persoană fizică, precum și suma impozitului acumulat. Ar fi mai ușor să se aplice o scară de rate regresivă nu în raport cu veniturile acumulate ale angajaților individuali, ci pentru organizație în ansamblu. Pe de altă parte, această scară de calcul a plăților nu contribuie la rezolvarea problemelor de reducere a tensiunii sociale, ci, dimpotrivă, o întărește, încălcând principiul echității și tensiunii egale în colectarea impozitelor și mărind decalajul veniturilor primite. de anumite grupuri de populaţie.

Dacă încercați să introduceți o cotă unică de plăți în cadrul Taxei Sociale Unificate, indiferent de cuantumul venitului, se creează premisele pentru reducerea limitei superioare a ratei fără a compromite formarea fondurilor sociale bugetare. Reducerea poverii fiscale va duce la o reducere a costului produselor (lucrări, servicii) în sectorul întreprinderilor mici și mijlocii, o creștere a profiturilor și o creștere a veniturilor fiscale la buget. În același timp, disponibilitatea fondurilor suplimentare de la producător va extinde posibilitățile de investiție în producție nouă sau reconstrucția și extinderea acesteia.

Calculele complicate conform Taxei Sociale Unificate este dreptul angajatorilor de a face cheltuieli în mod independent pe cheltuiala Fondului Federal de Asigurări Sociale al Federației Ruse. Ar fi mai corect să se stabilească o procedură în care toți plătitorii plătesc integral întreaga sumă a contribuției acumulate la Fondul Federal de Asigurări Sociale al Federației Ruse și apoi să primească rambursarea cheltuielilor lor de la fondul însuși. Acest lucru va facilita controlul în timp util și complet asupra cheltuirii fondurilor din fond.

Cu toate acestea, impozitul social unificat nu este cu adevărat unificat. Baza de impozitare a fondurilor se calculează separat pentru fiecare fond, iar impozitul se plătește fiecăruia dintre acestea în ordine de plată separate. Legiuitorii ar putea combina contribuțiile la fondurile de asigurări medicale obligatorii într-o singură plată, care ar fi calculată la o singură rată și distribuită între ele de către autoritățile federale de trezorerie sau să stabilească o plată unică care să fie creditată la fondul teritorial și apoi, conform conform standardului stabilit de deduceri din veniturile sale, fondurile vor fi anulate într-un cont de fond federal. Acest lucru va simplifica calculul și raportarea impozitelor, va reduce numărul de ordine de plată și, în același timp, va reduce cantitatea de muncă contabilă și numărul de conturi personale la autoritățile fiscale.

Mass-media vehiculează de ceva vreme informații despre planurile guvernului rus de a reforma radical sistemul de colectare a impozitelor. Unul dintre motivele principale este criza economică.

La început, discuțiile despre reformele fiscale au fost inutile. Și pe 21 ianuarie, multe instituții media au difuzat informații că guvernul rus se gândește la posibilitatea înlocuirii primelor de asigurare cu o singură taxă socială (UST).

Să reamintim că taxa socială unificată exista deja în Federația Rusă, dar în 2010 a fost înlocuită cu contribuții la Fondul de pensii, Fondul de asigurări sociale și Fondul de asigurări medicale obligatorii. Acum, în cadrul elaborării unui plan anticriză, guvernul ia în considerare problema desființării acestor trei contribuții și revenirea la impozitul social unificat. Data probabilă de returnare a impozitului social unificat este 1 ianuarie 2017.

Potrivit estimărilor guvernamentale, Taxa Socială Unificată din 2017 va permite Serviciului Fiscal Federal să obțină controlul asupra fluxului de numerar de aproximativ 5,9 trilioane de ruble pe an, ceea ce reprezintă aproximativ 7,5% din PIB.

O revenire la impozitul social unificat va deveni deosebit de relevantă dacă partea obligatorie finanțată a pensiei este eliminată: dacă aceasta dispare, atunci conceptul de „contribuție” va fi lipsit de sens. Totodată, conform datelor preliminare, în cazul returnării UST, cota acestuia se va menține la nivelul actual al ratei generale a primelor de asigurare.

Argumentele adversarilor UST

În ciuda dorinței guvernului de a returna impozitul social unificat, această problemă nu a fost încă rezolvată pe deplin. Mai mult, în Duma de Stat, se pare că această decizie va întâmpina o mare rezistență. O serie de deputați au vorbit deja negativ despre acest lucru.

În special, vicepreședintele Dumei de Stat A. Isaev consideră că revenirea la impozitul social unificat este o decizie greșită. Într-un interviu acordat jurnaliştilor, deputatul a afirmat necesitatea păstrării contribuţiilor sociale şi necesitatea păstrării caracterului asigurator al veniturilor la bugetul de stat. Potrivit acestuia, în situația actuală, angajatul însuși este interesat să plătească integral contribuțiile pentru a calcula o pensie echitabilă. La rândul său, natura UST, conform lui Isaev, este fără adresa - această taxă este primită de stat sub forma unei plăți, iar statul direcționează apoi fondurile primite în scopurile pe care le consideră necesare.

V. Fedotkin, membru al Comisiei Dumei de Stat pentru buget și impozite, membru al fracțiunii Partidului Comunist, s-a pronunțat și el categoric împotriva introducerii impozitului social unificat. Într-un interviu acordat postului de radio Govorit Moskva, el a spus că numai surse de încredere de reînnoire a veniturilor prin producție și știință pot salva Rusia acum. În opinia sa, orice altceva este doar o pierdere de timp, incapabil să atenueze gravitatea situației. El a numit tranziția planificată la impozitul social unificat „o abordare greșită din punct de vedere conceptual”, spunând că „dacă transferați bani din trei pungi în unul, nimic nu se va schimba”.

Caracteristicile Taxei Sociale Unificate din 2017 în detaliu. Această pagină oferă informații despre cine este plătitorul UST și discută problema calculării acestui impozit.

Taxele sociale există în orice stat. În Rusia, existența unui impozit social unic din punct de vedere juridic s-a încheiat acum 6 ani. Dar orice contribuție de semnificație socială este încă numită prin abrevierea obișnuită UST. Pentru calculele impozitelor se iau atât venituri bugetare, cât și alte venituri. Anul viitor este planificată returnarea acestui tip de impozitare.

Rate UST în 2017, tabel va contine unele modificari pentru plata impozitului.

- La deducerea acestui impozit, suma nu este rotunjită.

- Indicator maxim - acest concept este folosit pentru a calcula sumele pe care un cetățean trebuie să le plătească la Fondul de pensii. Sintagma a fost pusă în uz și este prescrisă în Legislație. Reglementările fiscale locale au un design și o interpretare nouă. Acumulările către Fondul de asigurări medicale nu se vor modifica.

- În cazurile în care un cetățean lucrează pentru o perioadă scurtă de timp, își obține un loc de muncă, dar în curând renunță, iar valoarea câștigurilor este mai mică decât valoarea medie lunară de 3 luni, primele de asigurare nu vor fi încasate. Această regulă se aplică și în cazul unor călătorii de afaceri. Pentru a evita perceperea dobânzii la indemnizațiile de călătorie, trebuie să prezentați elementul de cheltuieli.

- În cazurile în care lucrează un cetățean de origine non-rusă, va fi necesară o contribuție obligatorie la fondul de pensii. Excepție vor fi angajații cu înaltă calificare.

- Există tot mai multe organizații care lucrează astăzi cu raportare electronică.

Impozit social unificat UST din 2017 necesare pentru a facilita atribuirea de către stat a pensiilor și a altor beneficii sociale. Datorită taxelor, instituțiile medicale pot oferi îngrijiri medicale gratuite.

Ce persoane juridice și persoane fizice trebuie să plătească UST

Componentele Taxei Sociale Unificate

Impozitul constă în trei plăți diferite:

- Contributii la Fondul de pensii din aproximativ o rată de 22 la sută,

- MHIF solicită plata a 5,1 la sută.

- Fondul de asigurări va necesita 2,9 la sută.

Astăzi, maximul pe care îl puteți plăti în fondul de pensii este de aproximativ 155 de mii de ruble. Rata dobânzii se modifică; depinde direct de cifra de angajamente.

Suma maximă pe 12 luni poate fi redusă. Sezonul următor, se recomandă aplicarea unei cote de 2,9% la plățile către Fondul de asigurări sociale pentru sumele acumulate mai mici de 718 mii de ruble. În cazul unui număr mai mare, se aplică rata zero a acestui fond.

Dacă contribuțiile la Fondul de pensii sunt mai mici de 796.000 de ruble, se va aplica o cotă de impozitare de 22 la sută, iar dacă suma este mai mare, rata va fi redusă la 10 la sută.

Ce se va schimba anul viitor pentru antreprenori

UST din 2017 pentru antreprenorii individuali este următorul: contribuțiile la fondul de asigurări sunt voluntare, dar sunt necesare contribuții de pensie și medicale. Pentru calcul se ia salariul minim.

Plățile pentru Fondul de asigurări medicale obligatorii se calculează folosind formula: 12 * 5, 1% *. Pentru PF, totul este la fel, doar rata este de 26 la sută.

Când un antreprenor câștigă mai mult de 300.000 de ruble într-un an, se fac plăți sociale de bază și încă 1 la sută pentru suma în exces.

Amânări și verificări

Întreprinderile care supraveghează organizațiile vor avea dreptul de a controla activitățile nu timp de 4, ci de 6 luni. Si de aceea:

- În cazul unei încălcări grave, inspecția trebuie efectuată rapid și măsurile luate imediat. Totul este înregistrat și confirmat de documentația relevantă.

- Când o organizație are filiale care lucrează cu încălcări, va dura mai mult timp pentru a clarifica circumstanțele și a căuta dovezi.

- Datele solicitate pot avea lacune, iar documentele pot conține erori.

- Deducerile de asigurare nu au fost făcute la timp, chiar dacă a existat un caz de forță majoră.

Atunci când un antreprenor individual se confruntă cu astfel de circumstanțe extraordinare, este necesară o solicitare pentru planuri de rate.

Impozit social unificat din 2017 pentru antreprenori rămâne neschimbată.